Expanding footprint

Updated: 2016-03-04 07:58

By Chris Peterson(China Daily Europe)

|

|||||||||

Record year set for Chinese overseas mergers and acquisitions

Chinese companies - large and small, private and state-owned - are embarking on a spree of overseas mergers and acquisitions, spurred by government policy that promotes foreign expansion.

The signs indicate that the M&A activity this year will break all records, even at a time of economic uncertainty.

But what are the targets? Where are they? And, more importantly, how are Chinese firms going to overcome the inevitable challenges?

Ministry of Commerce data suggest smaller rather than larger entities are behind the latest sudden surge. In January, China's nonfinancial outbound investment was $12.02 billion (11.04 billion euros), increasing 18.2 percent from a year earlier, almost three times the rate in December.

Of the country's total overseas direct investment in January, 92.5 percent came from smaller enterprises, up 175.2 percent on the same period last year.

More statistics from Morning Whistle Group show that private companies completed 76.78 percent of China's M&A deals in 2015, while state-owned enterprises accounted for 20.29 percent.

The target areas were technology, media and telecommunications, agriculture and food, and energy and mineral resources, the Whistle Group says. And that's expected to remain the same this year.

Commerce Ministry spokesman Shen Danyang puts the trend down to favorable Beijing government policies aimed at boosting cooperation between Chinese players and international companies.

Chinese investment in foreign manufacturing rose 87.8 percent year-on-year to $1.62 billion (1.48 billion euros) in January, with much of the money flowing into the telecom, electronic equipment, pharmaceuticals and automobile sectors, Shen says.

Meanwhile, Chinese investment in the United States soared to $1.56 billion in January, nearly four times the amount in the same month last year, according to the ministry.

So what are the factors driving this?

Plummeting commodity prices are making some foreign companies cheap to buy. Plus, many Chinese state-owned enterprises have the means to buy, while for private companies, big or small, historically low interest rates mean borrowing is easier.

There's another reason, too. The Belt and Road Initiative, seen by many as a key pillar in China's foreign trade drive, means government cash may well be available to SOEs to help fund acquisitions and make investments.

The Silk Road Fund, a government-owned investment vehicle, was launched at the end of 2014 with an injection of $40 billion. It aims to support infrastructure projects, mainly in Eurasian countries that lie along the proposed Silk Road Economic Belt and the 21st Century Maritime Silk Road routes between China and Europe.

More to the point, Chinese state and private companies see the Belt and Road Initiative as a clear signal that the government wants them to look overseas.

"A lot of SOEs are fairly cash-rich," Ben Cavender of China Market Research Group told nasdaq.com recently. "One of the issues they are running into is they're out of room to grow in their home market."

It was inevitable that the big deals would make headlines.

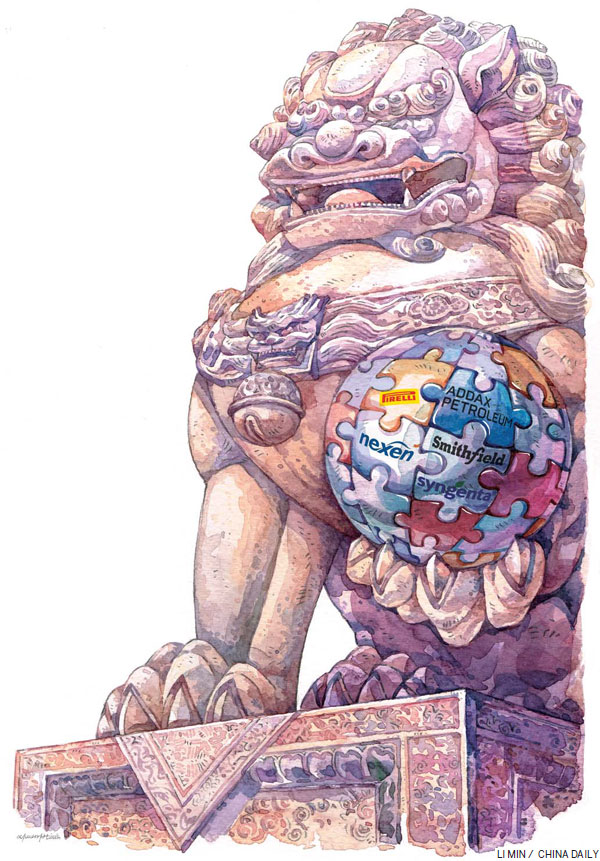

Probably the most eye-catching came in February, when China National Chemical Corp - or ChemChina - agreed to pay $43 billion for Swiss pesticide maker Syngenta. If shareholders and regulators approve the deal, it will be the largest-ever Chinese takeover of a foreign company.

The chemical company had already hit the headlines for buying Italy's premium tire maker, Pirelli, for $7.7 billion. The deal was funded in part by the Silk Road Fund, which took a 25 percent stake in the ChemChina unit set up to buy Pirelli's shares, nasdaq.com reported.

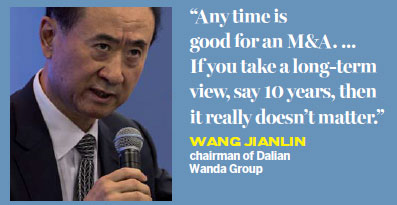

Wang Jianlin, chairman of Dalian Wanda Group and the world's 29th richest man, has forthright views on foreign acquisitions.

"Any time is good for an M&A," he told business students in a speech at Oxford University last week. "It's hard to determine when it's inexpensive and when it's expensive. It may be the case if you look at your investment on a two to three year time span, but if you take a long-term view, say 10 years, then it really doesn't matter."

Intense scrutiny

Merger activity can have its challenges, however.

Most analysts widely accept that the US, although a huge market, has a series of regulatory hurdles, as well as a Congress that at times seems highly protectionist.

For example, a move by Chinese investors led by GSP Ventures to acquire an 80 percent stake in Dutch company Philips' lighting and auto unit fell through after the powerful US Committee for Foreign Investment vetoed the move on security grounds. Philips has several US government contracts.

The committee is an interdepartmental agency that scrutinizes all foreign investment in the US, including takeovers and acquisitions. It reports to Congress and often focuses on national security implications. There have been a number of proposed deals in which the acquirer, faced with opposition from the committee, has walked away rather than mount an expensive legal challenge.

Zoomlion, the Chinese construction equipment maker, is eager to acquire Terex, a US crane maker, and has offered $3.3 billion, roughly double what Terex's shares were worth in January. But that may run into problems with the US Committee for Foreign Investment, according to Reuters.

ChemChina's bid to take over Syngenta is likely to face similar scrutiny, too, since the Swiss company does a lot of business in the US.

"The US claims to be a free country, but for investing, there are many complicated approval processes," Wang said in his speech in Oxford. "They can easily take back your license after 50 years.

"The United Kingdom and the US are equally important countries. I've invested $10 billion in the US because it's a big market, but the UK is the freest market in the world."

Despite challenges, the foreign merger route remains a desirable one for Chinese companies. Many executives see it as a way of acquiring know-how to help the country shift focus from "made in China" to "designed in China".

"M&A deals are an important ingredient in China's state-driven transition and development strategy," Danae Kyriakopoulou, senior economist at London's Centre for Economics and Business Research, told China Daily. "This is because Chinese companies need to acquire the know-how of the new growth sectors in order to support the economy's rebalancing away from being the world's hub for basic manufacturing and heavy industry and toward high-end economic activities, and M&As with companies of those more-developed economies in those sectors is a way to do that."

Chinese companies are being encouraged to seek merger targets abroad, buoyed by supportive government policies that have reduced paperwork and eased restrictions on overseas investment, adds Duncan Innes-Kerr, regional director for Asia at the Economist Intelligence Unit.

"The slowdown in China's economic growth has added momentum to the trend," he says. "Chinese firms are looking beyond the traditional fields that they used to invest in, like resources, and are now increasingly seeking to acquire talent, technology and access to high-margin markets in developed economies."

Other analysts agree. Professor Alan Barrell of the Centre for Entrepreneurial Learning at Cambridge University's Judge Business School says: "It makes enormous sense for a cash-rich economy such as China to spread its wings and grow internationally by acquisition, and to explore sectors as yet unexploited overall by M&As involving overseas companies and assets, notably technology, and not just real estate."

There are pitfalls, though. According to Kyriakopoulou, the biggest ones can come after a deal has been struck.

"These are chiefly to do with the understanding of different regulatory systems, and the clash of corporate cultures," she says.

In 2005, Qianjiang Ltd, a state-owned Chinese motorcycle manufacturer, acquired Italian scooter maker Benelli for 59.7 million euros, including 52.7 million euros of company debt. Although Benelli's chief technical officer was appointed as deputy managing director, he left after four years because of repeated clashes with a Chinese executive brought in to head the operation.

"Cultural differences emerged in terms of staff behavior and different management styles," concluded analysis of the takeover by China Business Review. It added, "Communication has been a key issue."

Ultimately, the issues were overcome, and Benelli QJ now makes and markets a successful range of scooters and motorcycles.

Wang at Wanda addressed the challenge of linguistic problems in M&As in Oxford. "English is our greatest challenge. We have a lot of senior employees in Wanda, but when going global in tourism, sports and entertainment, inadequacy in English is a huge challenge," he said.

"Although these people are good, they cannot be put to good use because of their lack of English language skills. When we recruit locally, we give preference to English-speakers and women. We receive a lot of expats in China, but they can speak good Chinese, so the language barrier is mitigated."

In terms of regulatory challenges, many law firms in London's financial district make a point of employing native Mandarin-speaking lawyers.

From a management point of view, many Chinese companies now accept that once a takeover or acquisition has taken place, it makes sense to keep most of the local management in place and to motivate them, rather than bring in Chinese nationals to replace them.

Wanda, for example, has a system of promising existing management 10 percent of the entity's profits as a way of encouraging growth and harmony.

Last but not least on the list of considerations is the effect of the fluctuating yuan on Chinese M&As.

Kyriakopoulou says the drop in the Chinese currency this year has surprisingly had little or no influence on M&A activity so far.

"If anything, we expect a potential continued devaluation of the yuan to actually intensify the incentives among Chinese companies to proceed with M&A deals, as they seek to acquire assets whose values are stable," she says.

"Fluctuations on China's stock market, on the other hand, could be potentially more damaging to the prospects of such deals by making it harder for Chinese companies to secure funding," she says, adding that many rely on bank loans, state finance or the so-called shadow banking sector. "The role of equity financing is pretty insignificant in China compared with its importance in American or European firms."

chris@mail.chinadailyuk.com

|

Ren Jianxin (right), chairman of China National Chemical Corp, makes a speech during the Swiss agrochemicals maker Syngenta's annual news conference in Basel on Feb 3. ChemChina has made a $43 billion bid for Syngenta. Arnd Wiegmann / Reuters |

( China Daily European Weekly 03/04/2016 page1)

Today's Top News

Trump, Clinton scoop up key wins on 'Super Tuesday'

British PM threatened with 'no confidence vote'

70,000 may become trapped in Greece

'Grow people' for long-term China-UK relations

Points of view

Small island makes a big difference

Rubio, Cruz gang up on Trump in debate ploy

'Invented-in-China’ products to the fore at MWC

Hot Topics

Lunar probe , China growth forecasts, Emission rules get tougher, China seen through 'colored lens', International board,

Editor's Picks

|

|

|

|

|

|