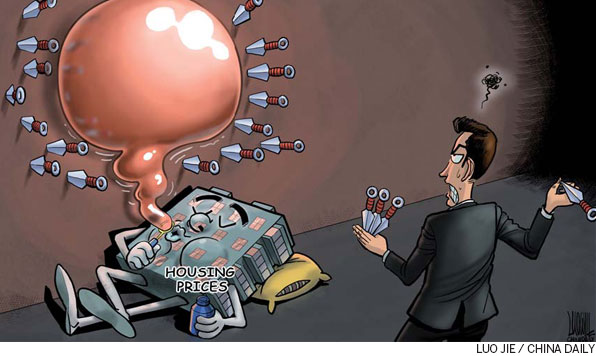

Keeping the lid on housing prices

Updated: 2014-01-31 15:25

By Zhu Ning (China Daily USA)

|

|||||||||||

Shiller's theories highlight the risks of asset bubbles in China and the need to take corrective action

Nobel laureate and Yale University professor Robert Shiller was one of the first global economists to talk about the runaway risks in China's spiraling property prices, a matter that has been of considerable interest in China recently.

Shiller, well known for his insights on global asset prices and extended research work on behavioral finance, macroeconomics and real estate, had during a visit to China mentioned that property prices were moving at a "dangerously high" pace. That comment, highly controversial back then, seems even more controversial now, given that real estate prices across most of China have increased by more than 50 percent, and by more than 100 percent in a few high-profile markets.

It is also worth noting that Shiller has not always been spot on with his predictions, especially those on the US real estate market. In 2005, Shiller faced considerable skepticism when he predicted that the real estate bubble would burst in the US. The US real estate market started showing bubble signs two years later, and this was followed by five years of continuous price decline.

However, the problem with the Chinese real estate market is far more complex.

In the last three decades, China has emerged as one of the greatest economies in the world and its citizens are enjoying a lifestyle comparable to those in countries with far higher incomes. At the same time, the desire to lead comfortable lives has prompted Chinese people to also highly value the quality of their residence.

Furthermore, since urbanization is an important driver for the next stage of economic growth, it is natural that more people will migrate to the bigger cities, which further boosts investors' confidence in real estate as an asset class.

On the other hand, Shiller's research on real estate can offer at least the following perspectives on the Chinese real estate market.

Based on his work and some other research carried out in the Netherlands, there is little evidence that real estate as an asset class can outperform a country's long-term inflation. In this sense, real estate may not be as attractive as equities in terms of investment returns.

At the same time, the research also shows that the current methodology used by China to calculate the appreciation level of the real estate market is flawed, as it does not account for the fact that the sample size for real estate transactions has changed over time. This is a particularly serious problem for the Chinese real estate market because of the hastened pace of real estate development in urban expansion. Based on some of the author's calculations, such a bias may result in an understatement of housing market appreciation by more than 100 percent.

Further, like many other asset classes, such as equities and fixed income securities, the value of real estate is primarily determined by its fundamental value, in this sense, the rent generated from leasing. Based on such criteria, rental yields from Chinese real estate are appallingly low, when compared to international average, and also meager compared to Chinese data from five years ago.

Put differently, although housing prices have increased substantially over the past five years, rents, or the dividends from owning real estate as investment assets, have not increased in tandem. One of Shiller's major research contributions is that, based on his research into the real estate and equities market in the US, he shows convincingly that there cannot be too much deviation between asset prices and the fundamental value. If that does happen, then bubbles could form, Shiller has said.

Shiller, however, admits that bubbles do not necessarily pop immediately after they are sighted and it is difficult to predict when they would do so. As a matter of fact, the formation and escalation of bubbles may indeed reinforce people's belief in assets that are already in bubble price range. This is especially the case for real estate, given that there are limited ways for investors with bearish views to "short sell" in the real estate market.

However, Shiller points out that, as long as the price greatly exceeds the fundamental value of an asset, it is just a matter of time until the bubble bursts. By that time, the longer the bubble lasts, the longer it may take the economy to recover from the burst.

The author is a faculty fellow at the International Center for Finance, Yale University; and deputy director of the Shanghai Advanced Institute of Finance, Shanghai Jiaotong University. The views do not necessarily reflect those of China Daily.

Related Stories

Homing in on affordable housing units 2014-01-25 08:06

Rural houses to be covered by system 2014-01-08 16:51

Housing is largest worry of Chinese: survey 2013-12-30 19:48

Secondhand housing market sees chill in Dec 2013-12-26 09:42

China plans to build more affordable housing 2013-12-24 19:12

Today's Top News

Xi extends Lunar New Year greetings

London goes all-out to ring in Lunar New Year

Chinese family infected with H7N9

HK slaps sanctions on Manila

More Chinese set to travel overseas

Experts call for detailed H7N9 rules

Huawei pledges more jobs in Europe

HK confirms H7N9 case, to cull 20,000 poultry

Hot Topics

Lunar probe , China growth forecasts, Emission rules get tougher, China seen through 'colored lens', International board,

Editor's Picks

|

|

|

|

|

|