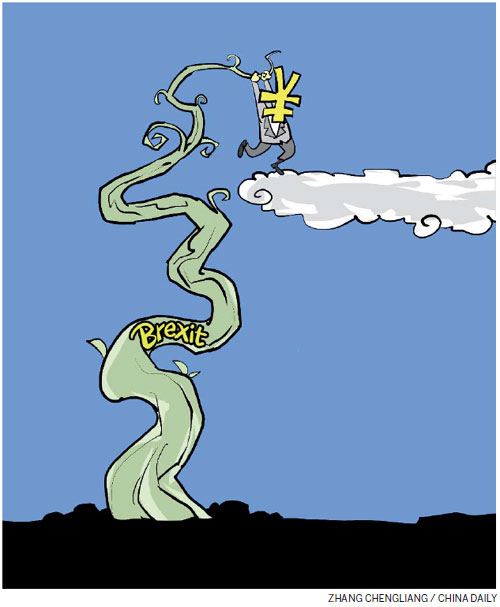

Brexit a break with euro-negativity

Updated: 2016-07-22 07:35

By Ding Jianping(China Daily Europe)

|

|||||||||

While negative interest rates stagnate European monetary policies, leaving may help the UK find more development modes

The world is full of gloom-mongers about the pound since the result of Britain's EU referendum. Yet Brexit didn't happen in a day - it is a culmination of internal reasons.

Monetary policies in Europe are stagnated by negative interest rates, so leaving the bloc is Britain's attempt to find a more sustainable development mode and to protect itself from the forthcoming global economic recession. From now on, the pound can fluctuate as it needs, which can ensure competitiveness for the country's exports and help avoid a negative interest rate.

London's independence as a financial center will actually boost the renminbi's development in the offshore market. Maintaining an interest rate that is floating downward and keeping a positive rate is a possible mode for Britain.

The EU has been stuck with negative interest rates for a long time, and there's no signal that this will change anytime soon. Britain has the world's largest foreign exchange center. If that too is hit by negative interest rates just like the EU, then as an international financial market the city's interest rate will also turn negative, and its function in pricing financial derivatives will be affected. With the US Federal Reserve on the path to lifting interest rates, this would certainly place London's role in global finance in jeopardy.

Although people's views vary over what effect negative interest rates have on economic development, after decades of experience we can see that the faults have become more obvious. It is a practice for unusual times, and cannot apply to "normal" periods. A negative interest rate doesn't bring more capital to the real economy. Look at Japan over the past 20 years and the EU over the past five - the real economy hasn't recovered.

Britain, an island country, has seen its manufacturing industries move to other regions, while the remaining industries are mostly services, especially in the finance sector. For a country where the core competitiveness is the finance industry, ensuring that it doesn't enter a period of negative interest rates is a smart choice.

The falling pound will benefit Britain's competitiveness in exports, but it won't want to follow in the footsteps of Japan. In the 1980s, Tokyo was the Asia-Pacific region's financial center, but negative interest rates and the appreciation of the yen saw the city lose its status.

In Tokyo's offshore currency market, the yen was actually marginalized, while transactions done through dollars were very active. So the best solution for the pound, which has not yet seen a negative interest rate (the rate right now is said to be 0.5 percent), is to depreciate and maintain a positive rate.

Brexit has disturbed the US Fed's pace in raising the interest rate, and so too could the renminbi if its interest rate floats downward.

In the International Monetary Fund's reserve currency basket, there are now two sides: the EU and Japan, which apply negative interest rates, and China and US, which have positive interest rates. Britain has taken its side. The pound's interest rate, without much restraint from the EU, will benefit London in its role as an international financial center.

A positive interest rate will help strengthen the British currency's international status, while RMB internationalization will also require interest rates to be sound. Otherwise non-Chinese residents who hold yuan-denominated assets will not be able to collect their earnings. Zero interest rates will speed up carry trade transactions.

A currency carry trade is a strategy in which an investor sells a certain currency with a relatively low interest rate and uses the funds to purchase a different currency yielding a higher interest rate, according to Investopedia.

What's different from Britain is that China is not an island country, and its manufacturing sector still plays an important role in its economy. With the increasing elasticity of the RMB exchange rate, the best choice is for China to keep to the transparent interest rate under the China Foreign Exchange Trade System, while keeping its normal interest rate.

On the one hand, it needs to ensure its market share among main trade partners; on the other, it needs to avoid being dragged into a negative interest rate situation, as well as continuing to improve competitiveness in exports and push forward progress in the internationalization of the renminbi.

London is the biggest offshore RMB market besides Hong Kong, and after Brexit, London's independence as a financial market will be stronger. While keeping a floating downward pound and normal interest rate, London's position of being an international financial center will not be weakened. Instead, it will help improve the development of the RMB offshore market. In particular, it will become a testing market to cultivate RMB financial derivatives.

Meanwhile, a normal interest rate and a floating downward exchange rate will help with the realization of the Shanghai-London stock connect.

It's estimated that the EU's negative interest rate will continue to fall, while the US Fed's pace to lift the interest rate is irreversible, so the fluctuation in the RMB exchange rate before the G20 summit in September will draw the world's attention.

China's ability to maneuver between negative interest rates in the EU and Japan and the positive interest rates of the US and Britain will be tested.

The author is a member of the academic committee at International Monetary Institute of Renmin University of China. The views do not necessarily reflect those of China Daily.

(China Daily European Weekly 07/22/2016 page10)

Today's Top News

French president urges Britain to begin EU exit talks

Turkey to restructure its army after coup attempt

UK to keep close economic ties with Germany: May

China's Fosun buys UK's Wolves for 45 million pounds

Rio 2016: Russia loses doping appeal

Brussels police: Bomb aleart was false alarm

May takes center stage in parliament's box-office show

Turkey's failed coup to consolidate Erdogan's power

Hot Topics

Lunar probe , China growth forecasts, Emission rules get tougher, China seen through 'colored lens', International board,

Editor's Picks

|

|

|

|

|

|